Icahn vs Buffett in Occidental Petroleum

November 21, 2023 | InsiderSentiment.com Team

Intro

Occidental Petroleum Corp. (NYSE: OXY) is in a curious spot lately. Recently, we noticed that two of its well known insiders, Carl Icahn and Warren Buffett, have taken seemingly opposite strategies based on their insider trading activity in the stock. Carl Icahn has sold large volumes while Warren Buffett is buying large volumes of OXY shares. We found this intriguing as insiders usually agree with each other and trade in the same direction. We decided to take a deeper look into OXY. Which of the two legendary investors is likely to come out on top? Let’s explore.

First, we’ll share some background information on OXY’s business to give proper context. Then we’ll jump right into our valuation analysis. Then we’ll take a deeper look at the insider trading activity and see how likely it is that electric vehicles put a dent in OXY’s business. Lastly, we’ll wrap it all up and tell you exactly why we think Buffett will come out on top in the long run.

OXY Background

OXY’s principal businesses consist of oil and gas, chemical and midstream and marketing. The oil and gas segment explores for, develops and produces oil (which includes condensate), NGL and natural gas. OxyChem primarily manufactures and markets basic chemicals and vinyls. The midstream and marketing segment purchases, markets, gathers, processes, transports and stores oil (which includes condensate), NGL, natural gas, CO2 and power. It also optimizes its transportation and storage capacity, and invests in entities that conduct similar activities, such as WES. The 2022 revenues for OXY were $36.6B with COGS of $19B for a gross profit of $17.6B.

OXY Stock Price History

The last 5 year stock price history for OXY is shown below. OXY’s stock price dipped below $10 following the COVID shutdowns but has since retraced back up to between $60 and $80 a share. At the time of writing it sits at near $61.

Analyst Ratings

Analysts are moderately bullish on OXY, with 10 buy, one overweight, 17 hold, 0 underweight and one sell. Consensus is overweight.

Oil Exploration

Currently, total production is 423 Mbl, while total proved reserves ($3.8Bbl) are enough to sustain OXY’s production at current rates for nine years without any new discoveries. OXY spent about $5B on exploration and development in 2022 and added a net (after production) of 300Mbl to its proved reserves. This is a crucial fact that we will revisit later.

Valuation Analysis

We now go to the discounted cash flow analysis in order to value OXY’s stock price and see if it agrees or disagrees with either Icahn’s or Buffett’s analysis. We start by projecting 2022 figures outward and then repeat the analysis under slightly different conditions, going all the way down to our most bearish, worst case scenario, where OXY makes no new oil discoveries and simply sells off its existing reserves.

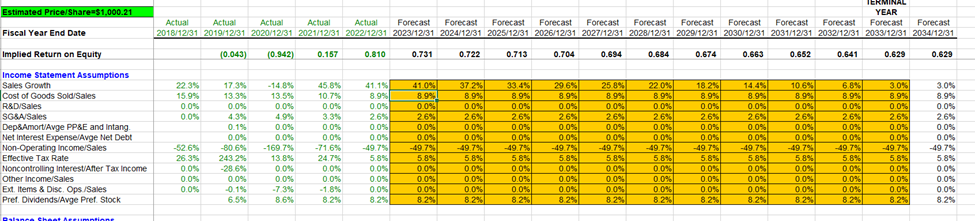

Projecting the Recent Year Out

Using the information from the 2022 10K, we can forecast the free cash flows for OXY for the next ten years in order to value the stock. For year 11 and beyond, we fit a Gordon’s constant growth formula as follows: Equity Value in year 11 = FCF (equity in year 10) / (R – g), where R is equity required rate of return (taken at 10%) and g is the perpetual constant nominal growth rate (3%).

Using a 41% sales growth forecast for 2023 and bringing this sales growth rate back to 3% over ten years gives a per share valuation of $1,000. This seems quite unrealistically optimistic since 2022 was an exceptionally good year for OXY and these great results should not be expected to last for ten years. While OXY may be undervalued, this estimate of $1000 a share seems too high. See below for details.

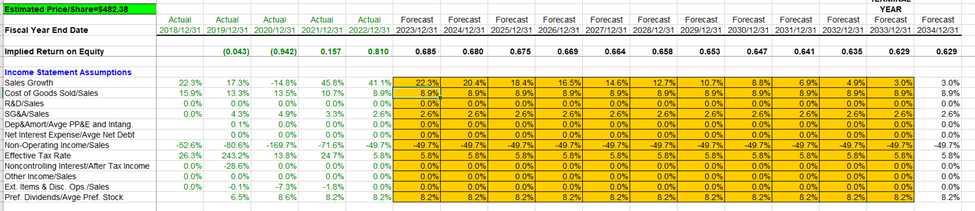

Using Last Five Years

We repeat the analysis using the last five years of performance instead of just 2022. Now, the five-year average sales growth rate is 22.3% and we lower that down to 3% over the next ten years. Under these assumptions, the warranted stock price falls to $482. Still high, but better than $1000 using only 2022 growth rate.

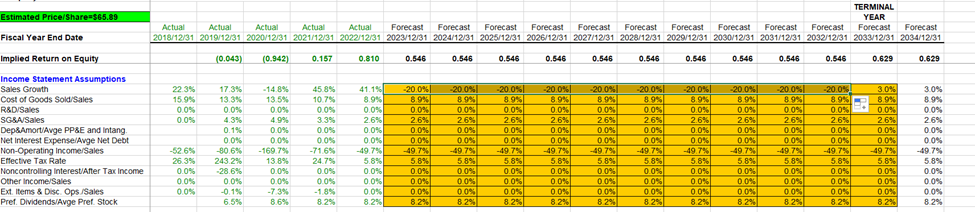

Deriving The Current Market Price

Now we reverse engineer the DCF model and solve for the constant sales growth rate that would give us the current market price. In order to justify the recent stock price of $61, the implied sales growth rate for every single year over the next ten years must equal at least -20% or worse. Hence, implied sales levels must go down from $36B in 2022 to just $4B in ten years. This is quite unrealistic. There is no possibility that OXY sales will go down to $4B or the implied oil price in ten years will go down to under $10 per barrel. Even under the worst-case demand scenario, oil price should not decline to just $10 or below per barrel over the next ten years. Thus, at the current valuation of $61 a share, the market is too pessimistically pricing OXY. Warren Buffett seems to be right again. Details are provided in the charts below:

Worst Case Scenario

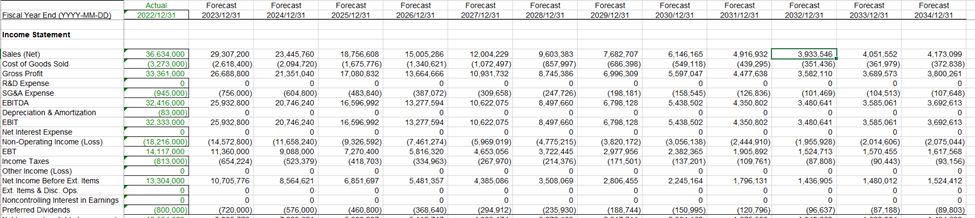

Finally, we also calculate the stock price under the worst case scenario. Suppose OXY stops exploring and sells all of its currently proved reserves until they are empty. Under this (unlikely) approach, OXY’s current reserves will be spent in 9 years, with zero growth and zero exploration and development expenses. Sales after 9 years are set to zero. Even before any cost savings, warranted stock price based on just depleting current oil and gas reserves is $101 per share. Again, this worst case bear scenario makes the current price of $61 seem far too low.

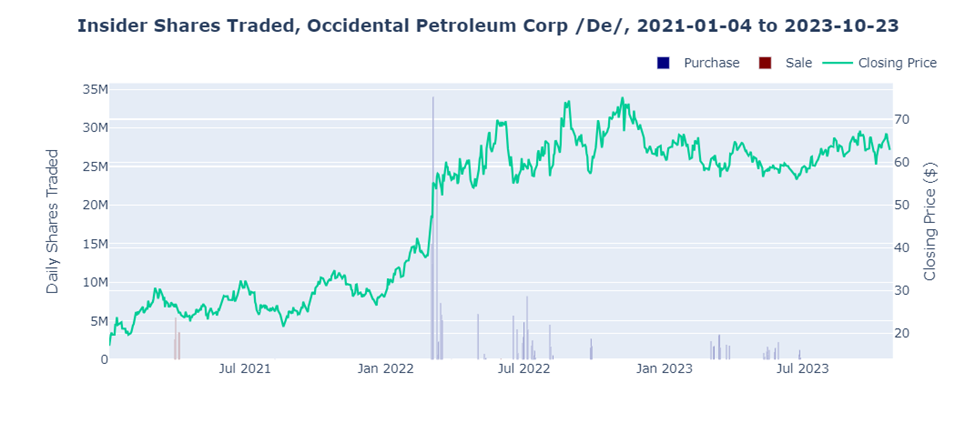

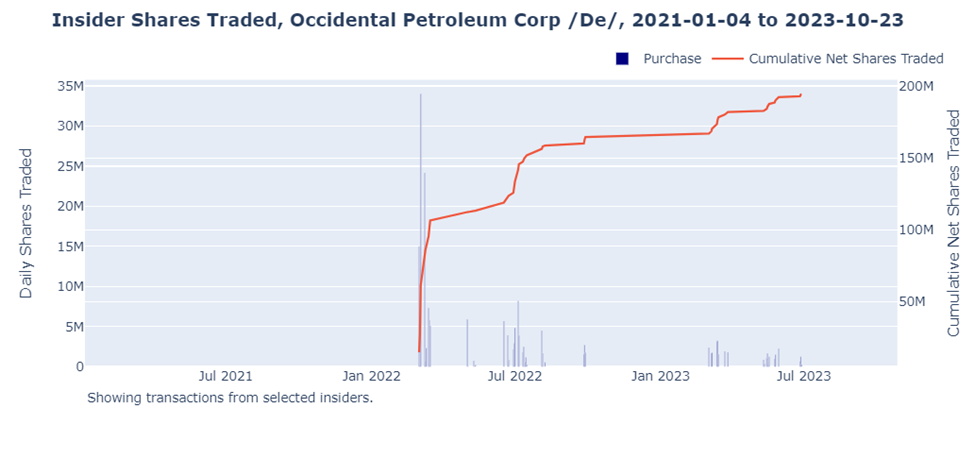

Insider Trading Activity

Icahn and Buffett have dominated the recent insider trading activity in OXY. While Icahn made all of his sales in a small window of spring 2021, Buffett has made regular purchases since March of 2022, right as the stock price ticked back up following the slump after COVID shutdowns occurred. The four other insiders have made only one insider trade each in OXY and they are split down the middle with two sales and two purchases. Buffett’s purchases seem to be related to his long-term outlook on OXY rather than exploiting short-term price movements, since he is happy to continuously be buying shares.

Growth of EVs

The likely explanation for the low valuation of OXY and potentially the opposite strategies we are seeing with respect to Icahn and Buffett is that investors are overly optimistic about the prospects for electrification and expect the demand for oil to drop sharply. Demand for oil in large part will depend on the rate of replacement of internal combustion engine vehicles with electric vehicles. Warren Buffett asserts that if EVs become half of the cars on the road in the US, that would seriously affect demand for oil and thus OXY’s prospects. Current figures are that the EV production for full year 2022 was 1M, while there are about 275M total vehicle registrations. We capped EV production at 18M (where EVs would represent all cars purchased), EV life at 10 years, and 9 M EVs (including hybrids) on the road today. Based on these numbers, it will take about 25 years for EVs (177M) to reach half of all registrations (352M). The takeaway is that EVs will not replace even half of all cars on the road for a long time. Thus, the basis for a sharp drop in the demand for oil seems to be overblown.

In Summary

As Buffett argued, it seems that due to the current popularity of EV technology, many investors are pivoting away from oil and gas stocks resulting in a severe undervaluation of the stocks of these companies like OXY. However, it does not look like oil and gas is not really threatened by electric technology all that much, especially over the next 20 years. This probably explains why Warren Buffett is buying up OXY and this is corroborated by the other consistent insider purchases which we suspect are driven by the long-term outlook for OXY based on the factors we’ve outlined here. We suspect that Warren Buffett is likely to win this battle with Carl Icahn.

Authors’ disclaimer: This article expresses the authors’ opinions. None of the authors have any business relationship with the company whose stock is mentioned in this article. None of the authors have any stock or derivative position in the company mentioned in this article, nor any plan to open such a position within 72 hours. Neither this article nor anything contained herein constitutes any recommendation or advice as to whether any investment or investing strategy is suitable for any particular investor. Consult with your licensed financial advisor before making any investment decision.